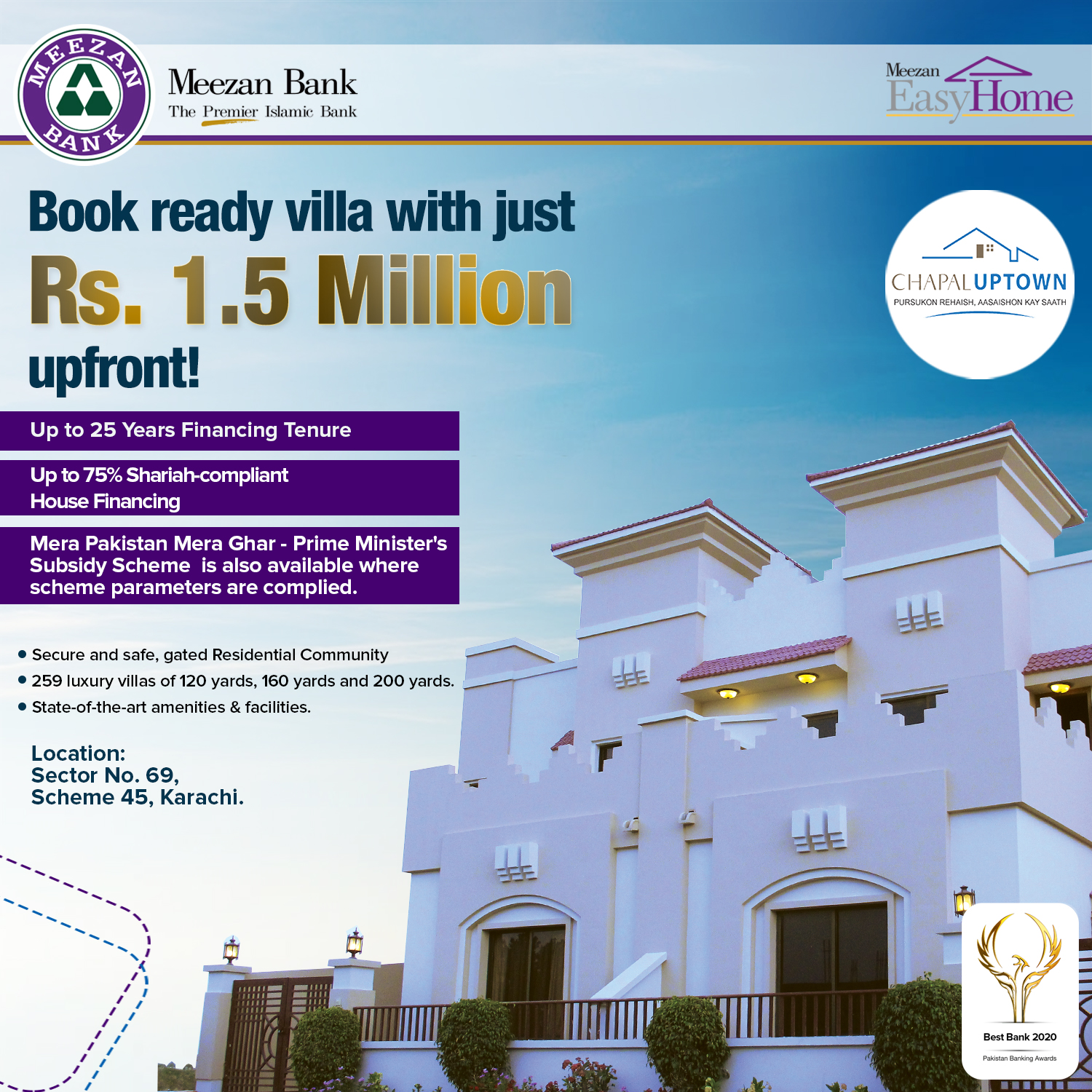

Easy Home is a completely interest (Riba) free solution to your home financing needs. Unlike a conventional house loan, Meezan Bank’s Easy Home works through the Diminishing Musharakah where you participate with Meezan Bank in joint ownership of your property. The nature of the contract is co-ownership and not a loan. This is because the transaction is not based on lending and borrowing of money but on joint ownership of a house. Meezan Bank, thus shares the cost of the house being purchased. Creating joint ownership and then gradually transferring ownership to the consumer instead of simply lending money is the major factor that makes Easy Home Shariah-compliant.

With Easy Home you participate with Meezan Bank in joint ownership of your property, where the Bank will provide a certain amount of financing. You agree to a monthly payment to the Bank of which one component is rent for the home, and another for your equity share. In fact, the total monthly payment is reduced regularly as your share in the property grows. When you have made the full investment, which had been agreed upon, you become the sole owner with a clear title to the property.

Pakistani National (Resident or Non-Resident) as per the Bank’s policy

In case of applicant & co-applicant (with income clubbing):

In case of co-applicant (without income clubbing):

*For salaried person, the age of applicant must not exceed 65 years OR retirement age, whichever is earlier. (Normal retirement age will be considered as 60 years if not mentioned otherwise).

*Spouse, parents, adult children, brothers & sisters only.

*Self Employed Professional includes doctors, engineers, auditors & architects.

**In case of contractual employees, minimum PKR 100,000 per month will be required

Minimum 3 years in current business / industry.

Note: In line with State Bank of Pakistan's regulatory requirement, negative history (i.e. overdue/ late payment/ write-off/ waiver) of consumer/individual customers will be reflected in e-CIB reports for two years after settlement.

At Meezan Bank, the profit margin is directly correlated to market trends to provide a competitive product to our customers. Shariah allows the use of any conventional market factor as a benchmark to determine the profit rate of a particular product. The mere fact that the applied profit rate of our product is based on similar factors used in determining the applied rate of interest of a mortgage does not render the transaction or the contract invalid from the Shariah perspective, and neither does it make the transaction an interest-bearing one. On the other hand, it is the underlying structure of the product that determines its Shariah compliance.

Fixed – 1st Year: K * + 3.00 % p.a

Annual Re-pricing: K ** + 3.00 % p.a.

(Floor 8.00% p.a. and Cap 30% p.a.)

* For first year Fixed Rate, 'K' denotes KIBOR (Karachi Inter Bank Offer Rate), announced on 1st working day of each calendar month.

** Applicable KIBOR will be 12-month KIBOR announced on first working day of the month of profit rate revision.

Fixed rate of 18.99% for the first 3 years, followed by a variable rate* for the remaining years.

*Rent/Rental will be annually revised on the anniversary of the financing facility.

**Offer valid until July 31st, 2024

Fixed – 1st Year: K * + 4.00 % p.a

Annual Re-pricing: K ** + 4.00 % p.a.

(Floor 8.00% p.a. and Cap 30% p.a.)

* For first year Fixed Rate, 'K' denotes KIBOR (Karachi Inter Bank Offer Rate), announced on 1st working day of each calendar month.

** Applicable KIBOR will be 12-month KIBOR announced on first working day of the month of profit rate revision.

Fixed rate of 18.99% for the first 3 years, followed by a variable rate* for the remaining years.

*Rent/Rental will be annually revised on the anniversary of the financing facility.

**Offer valid until July 31st, 2024

Meezan Bank’s Easy Home works through the Diminishing Musharakh and conforms to Shariah laws specifically related to financing, ownership and trade. The nature of the contract is co-ownership and not a loan because the transaction is not based on lending and borrowing of money but on joint ownership in a house. Meezan Bank shares the cost of the house being purchased. Creating joint ownership and then gradually transferring ownership to the consumer instead of simply lending money is the major factor that makes Easy Home Shariah-compliant.

With Easy Home the Bank will finance up to 65% and 75% of the property value to businessmen and salaried individuals. The customer agrees to a monthly payment to the Bank, part of which is for use of the house and part for purchasing the bank’s share in the house. When the customer has made the full payment which had been agreed upon, he become's the sole owner with a free and clear title to the property. The profit charged by the Bank is therefore payment for use of its share of the house during the life of the contract.

Submit a filled & signed application form to Meezan Bank. Submit the required cheque for Processing Fee & External Agency costs.

Meezan Bank will verify your residential/office addresses.

For Salaried Self Employed professionals / Businessman, Meezan Banks will conduct necessary credit assessments and associated due diligence based on provided information. (Income Estimator on Meezan Bank's panel conducts income estimation and submits report to the bank)

Meezan Bank will obtain a legal opinion on the property documents provided by you

Meezan Bank's appointed valuation agency will evaluate the property to determine its market value

After you have fulfilled all Meezan Banks credit requirements, the bank will give you a conditional offer letter.

After approval of the case, you are required to open an account at Meezan Bank.

After completion of these steps and approval of your case, you will be required to come to Meezan Bank for signing of the Islamic House Finance Agreement and other legal documents

A Meezan Bank officer & authorized lawyer will accompany you and the seller of the property to the appropriate bank (incase of BFT) or registrars office for Property transfer. Original Property Documents will be handed over to the lawyer who, after verification of the documents, will hand over the pay-order to the banker or seller and will then complete the legal formalities on Meezan Bank's behalf

Must be a Pakistani national

Buyer, Builder, Renovation & Replacement

Salaried Individuals

100% co-applicant income club in case of spouse.

25 to 60 years. (Maximum 60 years at the time of maturity)

25 to 70 years. (Maximum 70 years at the time of maturity)

Minimum income must be equivalent to PKR 250,000/- or above.

Two years (minimum) regular experience in same industry. At least one year work experience in existing job in the same country.

3 to 20 Years.

PKR 0.5M - PKR 50M.

| Type of Charges | Salaried | Businessmen |

|---|---|---|

| Processing Charges | PKR 8,000 | PKR 8,000 |

| FED on Processing Charges@ 16%** | PKR 1,280 | PKR 1,280 |

| Legal Report Charges | At Actual | At Actual |

| Property Valuation Charges | At Actual | At Actual |

| Income Estimation Charges | N/A | At Actual |

(Regional Sales Manager - South)

Cell No: 0301-8242468 & 0331-2235002

E-mail: [email protected]

3rd Floor, Plot No. 42C, 22nd East Street

Phase I, DHA, Karachi

PABX: 021-38103500, 37133500 Ext: 1484

(Area Sales Manager - Lahore)

Cell No: 0304-0920521

E-mail: [email protected]

Address: Gulberg Branch, 60 Main Boulevard

Gulberg - II, Lahore

Dir. No: 042-35757435-6

PABX: 042-35879870-2

(Regional Sales Manager - North)

Cell No: 0304-0920524

E-mail: [email protected]

Address: Consumer Banking Center I Meezan Bank Limited,

Buland Markaz | Blue Area, Islamabad

Dir. No: 051- 2270321

(Area Sales Manager - Faisalabad)

Cell No: 0300-7203505

E-mail: [email protected]

Address: Meezan Bank Limited P-907-B, Saleemi Chowk

Peoples Colony # 01, Faisalabad

Dir. No. 041-8711963

(Area Sales Manager - Multan)

Cell No: 0300-6380586 & 0304-1927526

E-mail: [email protected]

Address: Nawan Shahar LMQ Road, Multan.

Dir. No: 061-4781554

PABX: 061-4785604-07

(Area Sales Manager - Bahawalpur)

Cell No: 0300-6356323 & 0301-1189210

E-mail: [email protected]

Address: Dubai Chowk Branch, Bahawalpur

Fill out the form below and you will be contacted by a Meezan Bank representative.